Standards and Interpretations applicable at 30 June 2022

Now that interim final reports are being finalised for 30 June 2021, we present an overview of the IASB’s most recent publications.

Keywords: Mazars, Thailand, IFRS, IASB, EFRAG, IFRS IC, EU, IAS 34, IAS 8

22 July 2022

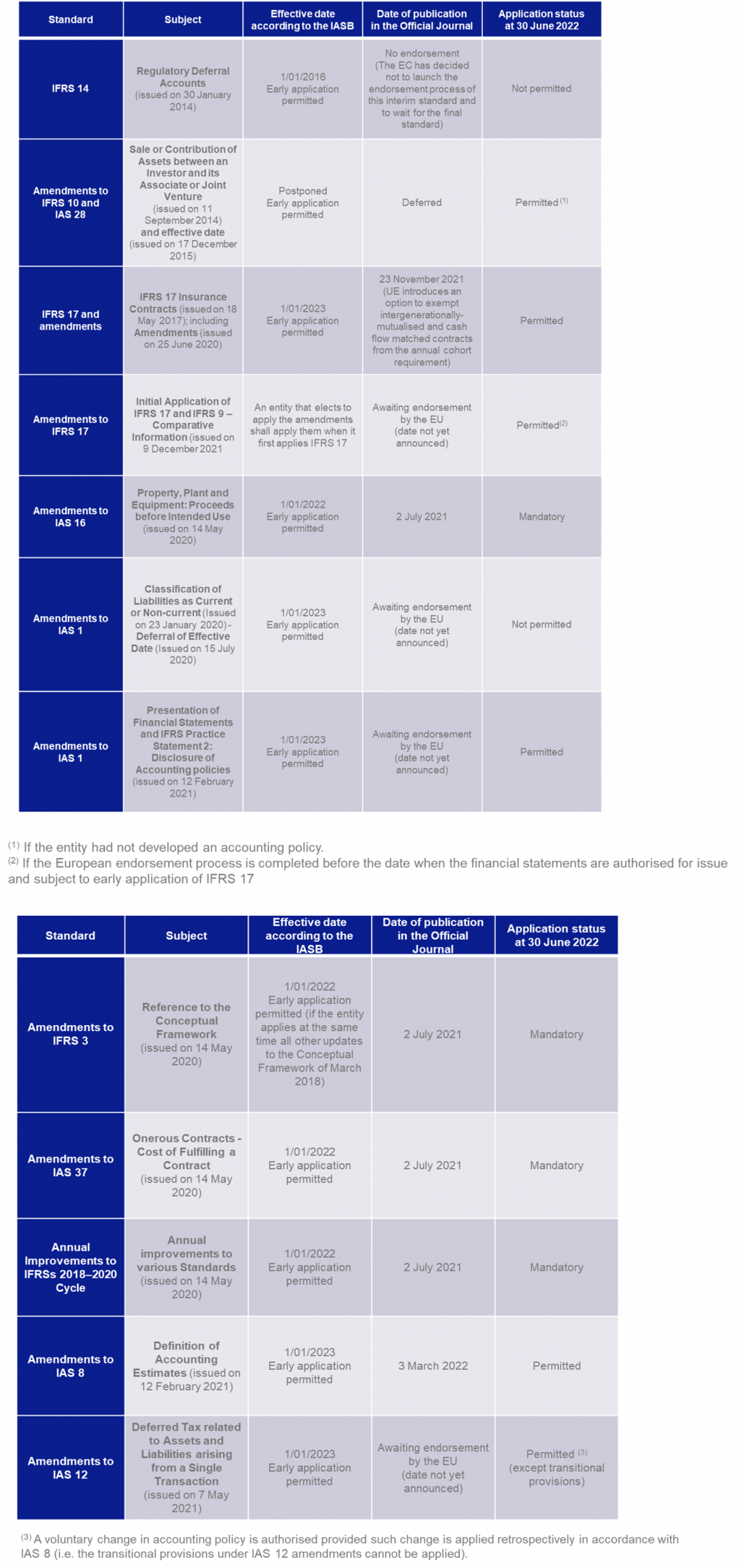

For each text, we clarify whether it is mandatory for this closing of accounts, or whether early application is permitted, based on the EU endorsement status report (position as at 2 May 2021, available on EFRAG’s website here).

As a reminder, the following principles govern the first application of the IASB’s standards and interpretations:

1. The IASB’s draft standards cannot be applied as they do not form part of the published standards;

2. The IFRS IC’s draft interpretations may be applied if the two following conditions are met:

- the draft does not conflict with currently applicable IFRSs;

- the draft does not modify an existing interpretation which is currently mandatory.

3. Standards published by the IASB but not yet endorsed by the European Union at 30 June may be applied if the European endorsement process is completed before the date when the interim financial statements are authorised for issue by the relevant authority (i.e. usually the board of directors);

4. IFRS IC’s Interpretations published by the IASB but not yet endorsed by the European Union at the date when the interim financial statements are authorised for issue may be applied unless they are in conflict with standards or interpretations currently applicable in Europe.

Remember that in accordance with IAS 8 the notes of an entity applying IFRSs must include the list of standards and interpretations published by the IASB but not yet effective that have not been early applied by the entity. In addition to this list, the entity must provide an estimate of the impact of the application of those standards and interpretations.

Regarding minor amendments and interpretations, it seems relevant to limit such list to only those amendments and/or interpretations which are likely to apply to the entity’s activities.

It should also be noted that under IAS 34 – Interim Financial Reporting, the changes in accounting policies required by new standards must also be disclosed in the interim financial reporting published in the course of the year.

Want to know more?

Tippawan Pumbansao Audit Partner Bangkok

Our services

Audit and assurance

Independence and Rigour that provides confidence and transparency for stakeholders and society.

Outsourcing

An outsourcing partner that helps you play to your strengths.